Churn Prediction - Comparing Multiple Models

Georgios Karaliolios

2024-03-21

Abstract

This project report delves into identifying critical factors and

the most effective predictive model for customer churn at a Dutch energy

provider, a pressing issue in the competitive European energy sector. By

meticulously analyzing a dataset of 20,000 customer observations, the

study executed a thorough data preparation process including outlier

removal and the introduction of a new variable for better understanding

customer behavior. The investigation compared various predictive models,

including Logistic Regression, Decision Trees, Gradient Boosting, and

others, concluding that Gradient Boosting outperformed the rest. Key

findings underscore the significance of service usage, relationship

length, contract length, and flexible contracts in influencing customer

churn. Notably, longer relationships and contract durations correlated

with lower churn rates. The report suggests that the energy supplier

could enhance customer retention strategies by focusing on long-term

relationships and stable contract terms, alongside developing energy

efficiency programs for high-usage customers, thereby fostering loyalty

and reducing churn.

Managerial Summary

This project is dedicated to identifying the key factors and the

most effective model for predicting customer churn for a Dutch energy

provider. This task is especially critical in the European energy

sector, where market liberalization has ramped up competition, making

customer retention maybe the most important focus for companies in this

sector.

The examined dataset consists of 20,000 customer

observations, carefully refined through a comprehensive data cleaning

and preparation process. This involved the identification and removal of

outliers, particularly in critical variables such as income,

electricity, and gas usage, to enhance the integrity of the analysis.

Additionally, a new variable is introduced to better understand customer

behavior, the “flexible_contract”, on which contracts could be

terminated at any time.

The baseline model for this study comprises

a logistic regression model and it is constructed based on the study’s

hypotheses, deriving from the literature review and the exploratory

analysis. As a result, it includes the variables gender, age, income,

relation length, electricity usage, gas usage, contract length, and

flexible contract. Subsequently, different methods are implemented to

test their performance and to determine the most important attributes

for the specific task. The methods under comparison are Logistic

Regression, Stepwise Logistic Regression, Decision Tree model, Gradient

Boosting, Random Forest, Support Vector Machine, and Neural Network. The

model that emerged as the better performing based on various evaluation

metrics is the gradient boosting model.

Regarding the most

important attributes, this study highlights several key variables

significantly impacting customer churn. Service usage, relationship

length, and contract length are the most influential determinants.

Notably, customers with longer relationships and more extended contract

terms exhibited lower churn rates.

In conclusion, the energy

supplier can tailor their customer retention strategies more

effectively, focusing on long-term relationships, and stable contract

terms, and develop energy efficiency programs for customers with higher

energy usage.

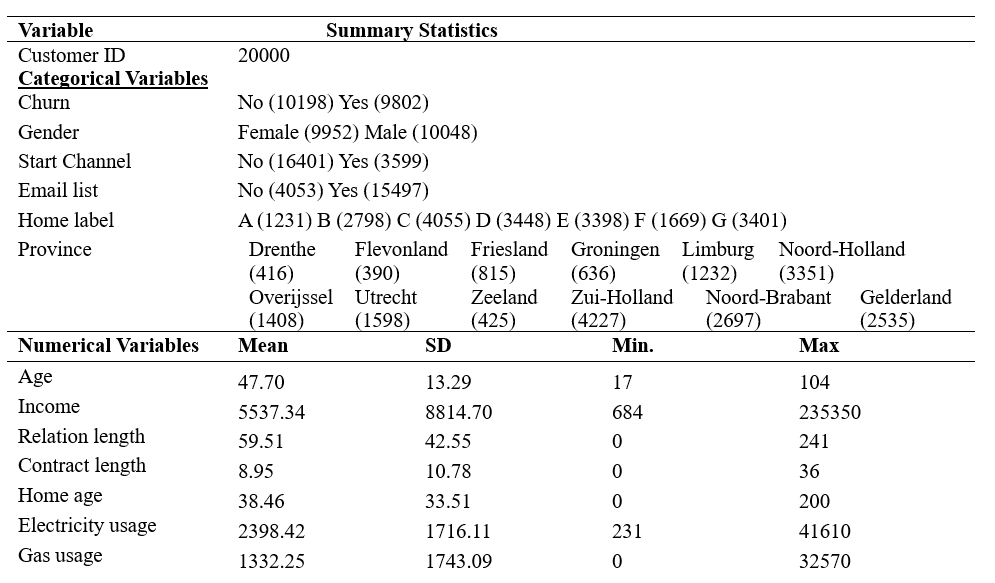

Data Description

The dataset, comprising 20,000 customer observations from a Dutch

energy supplier, underwent an initial summary check to identify any

potential anomalies. The examination revealed the absence of any missing

values within the dataset. The variables are converted to different

types, in order to give them the appropriate format. A descriptive

statistics table for numerical and categorical variables is then created

(Table 1). Based on this table, important insights are gained. It is

noticed that most of the customers are older and have moderate income.

Most of the customers are loyal as the mean relationship length is

almost 5 years.

*For a detailed description of the

different factors, refer to Appendix 1

Data Descriptives

Data Cleaning & EDA

The first step in the EDA and data cleaning process involves checking for missing values, while the second step focuses on converting factors into their appropriate forms

# Data Cleaning & Descriptives ----

# Reviewing missing values

for(col in names(data)) {

missing_values <- sum(is.na(data[[col]]))

print(paste("Column", col, "has", missing_values, "missing values."))}

# no missings

# Removing Customer_ID

data$Customer_ID <- NULL

# Convert the variables into the appropriate form

# columns to convert

factor_var <- c('Churn', 'Gender', 'Email_list', 'Home_label', 'Start_channel', 'Province')

numeric_var <- c('Electricity_usage', 'Gas_usage', 'Income')

integer_var <- c('Age', 'Home_age', 'Relation_length', 'Contract_length')

# Converting factor variables

for(var in factor_var){

data[[var]] <- as.factor(data[[var]])}

# Converting numeric variables

for(var in numeric_var){

data[[var]] <- as.numeric(data[[var]])}

# Converting integer variables

for(var in integer_var){

data[[var]] <- as.integer(data[[var]])}The data exploration process indicated the absence of missing values within the dataset. The subsequent step entails examining the distribution of numerical variables to identify any potential outliers.

# Convert data from wide to long format using pivot_longer

long_data <- data %>%

pivot_longer(cols = c(Electricity_usage, Gas_usage, Income), names_to = "Variable", values_to = "Value")

# Plot with ggplot2

ggplot(long_data, aes(x = Variable, y = Value)) +

geom_boxplot() +

facet_wrap(~ Variable, scales = "free_x", nrow = 1) +

labs(x = NULL, y = "Value") +

theme_minimal() +

theme(axis.text.x = element_text(angle = 45, hjust = 1))

Outliers in variables, “Income,” “Electricity_usage,” and “Gas_usage”

were identified through the use of boxplots. This method highlights data

points that lie outside the expected range. Further statistical analysis

of summary statistics, has indicated significant deviations in these

variables, especially in terms of their mean and standard deviations.

This was evident in the case of “Income,” where values ranged at

235,350, with a mean of approximately 5,537 and a substantial standard

deviation, indicating a widespread. Similarly, “Electricity_usage”

showed a maximum value of 41,610, exceeding the mean usage of about

2,398, and “Gas_usage” peaked at 32,570, which was much higher than its

mean of 1,332. These deviations highlight the presence of outliers that

could potentially affect the overall analysis. Thus, it is considered

that extremely high values in “Income”, Electricity_usage” and

“Gas_usage,” may not accurately represent the general customer base,

indicating anomalies, measurement errors, or data entry errors. Driven

by the necessity to maintain data quality, ensuring that the analysis

reflects the typical customer profile and is not skewed by extreme,

atypical values, we proceed to the removal of these outliers. The

methodology for the removal of these outliers is described below. By

plotting the boxplots, it is observed that income, electricity, and gas

usage have significant outliers and based on their values they were

deleted. The number of observations is diminished to 19699. Below, it is

explained analytically.

Income: All variables above value 30042 were deleted, as it was

determined that this is the point where the values experience a

significant breakpoint. This was done by calculating the point at which

the greatest difference between the values of the variable is noticed.

With only 60 variables (0.3%) having an income value above 30042, it was

determined that deleting them wouldn’t skew the data negatively, due to

the insignificant amount. Deletion was chosen over completion to

minimize noise, simplify and strengthen the models, and avoid

overfitting.

Electricity Usage: All variables above 9000 in

electricity usage were deleted. This was discovered through plot

analysis and studying the units at the change points, with sorting

employed for easier and clearer understanding. Given that only 117

variables (0.585%) had electricity usage above 9000, it was determined

that their deletion wouldn’t negatively skew the data, due to the

insignificant amount.

Gas Usage: All variables above 3209 were

deleted using the same method as with the income. With only 125

variables (0.625%) having electricity usage above 3209, it was

determined that deleting them wouldn’t negatively skew the data, given

the insignificant amount.

Age: It was chosen to remove all

values where the age is less than 18, as it logically doesn’t make sense

for someone who is not an adult to have a contract with the

company

Correlation Matrix

# Exploratory Analysis -----

## How many customers have churned

# Corelation Matrix

data_numeric <- data %>%

mutate_if(is.factor, as.integer) %>%

mutate_if(is.character, function(x) as.integer(factor(x)))

cor_matrix <- cor(data_numeric, use = "complete.obs")

melted_cor_matrix <- melt(cor_matrix)

unique_vars <- unique(c(melted_cor_matrix$Var1, melted_cor_matrix$Var2))

var_mapping <- setNames(seq_along(unique_vars), unique_vars)

melted_cor_matrix$Var1 <- var_mapping[as.character(melted_cor_matrix$Var1)]

melted_cor_matrix$Var2 <- var_mapping[as.character(melted_cor_matrix$Var2)]

melted_cor_matrix <- melted_cor_matrix %>%

filter(Var1 <= Var2) # Include the diagonal

# Create the Correlation heatmap Matrix

ggplot(melted_cor_matrix, aes(x = Var1, y = Var2, fill = value)) +

geom_tile() +

geom_text(aes(label = sprintf("%.2f", value)), color = "black", size = 3, check_overlap = TRUE) +

scale_fill_gradient2(low = "blue", high = "red", mid = "white", midpoint = 0, limit = c(-1, 1)) +

scale_x_continuous(breaks = var_mapping, labels = names(var_mapping)) +

scale_y_continuous(breaks = var_mapping, labels = names(var_mapping)) +

theme_minimal() +

labs(title = "Correlation Matrix Heatmap (Lower Triangle)", x = "", y = "") +

theme(axis.text.x = element_text(angle = 45, vjust = 1, hjust = 1))

The variables with the strongest negative correlations are age,

relationship length, contract length, flexible contract (the strongest),

and start channel, indicating that churn decreases as these variables

increase. Conversely, home age, electricity, and gas use show the

strongest positive correlations, meaning churn increases as these

variables increase. These being the variables with the strongest

statistical influence on churn, their relationship was studied more

closely. The relationships of each variable with churn are then examined

using plots and appropriate tests (chi-squared test and logit

regression), revealing significant associations with churn for all

variables.

Dependent - Independent Variables Relationship

## Discrete Variables

## Relation length (Significant)

ggplot(data, aes(x = Relation_length, y = Churn, fill = Churn)) +

stat_summary(fun = "mean", geom = "col") +

labs(title = "Mean Relation Length of Remaining vs Churned Customers") +

theme_bw()

## Start_channel (Significant)

ggplot(data, aes(x = Start_channel, fill = Churn)) +

geom_bar(position = "dodge") +

labs(x="Start Channel", y="Churn Amount", title="Churn per Start Channel") +

scale_fill_manual(values=c("#FF4136", "#2ECC40"), labels=c("No", "Yes")) +

theme_bw()

## Electricity usage (Significant)

ggplot(data, aes(x = Electricity_usage, y = Churn, fill = Churn)) +

stat_summary(fun = "mean", geom = "col") +

labs(title = "Mean Electricity Usage of Remaining vs Churned Customers") +

theme_bw()

The analysis of customer behavior reveals that a significant

portion of high electricity and gas usage customers have experienced

churn. Notably, customers with flexible contracts, indicative of shorter

relationship lengths, show a higher likelihood of churning. Furthermore,

the acquisition channels play a role in customer retention. The company

has acquired a greater number of customers online compared to phone

acquisitions. Interestingly, a higher percentage of customers acquired

online have churned, while a larger proportion of customers acquired

through phone interactions have remained loyal to the company.

Model Estimation and Evaluation

The baseline model in this study is a logistic regression model,

developed from the hypotheses generated through literature review and

exploratory analysis. This model incorporates variables such as gender,

age, income, relationship duration, electricity and gas consumption,

contract length, and the availability of a flexible contract. To

evaluate their efficacy and identify the key factors for this specific

task, various methods are tested, including Logistic Regression,

Stepwise Logistic Regression, Decision Tree model, Gradient Boosting,

Random Forest, Support Vector Machine, and Neural Network.

To determine the best-performing model, various metrics are employed.

The body of literature on churn management encompasses a wide range of

metrics for evaluating the effectiveness of models designed for

predicting customer churn. The Hit ratio helps to measure the model’s

accuracy and tries to correctly identify the positive cases of a

logistic regression. One limitation is that it doesn’t identify the

false positives of the model. The Top Decile Lift tells us how effective

the model is in ranking predictions. It does that by splitting the

predictions into deciles (10 groups of the same size) and comparing the

10th decile with a random selection or with another model. The Area

Under the Curve (AUC) is a metric used to evaluate the performance of a

binary classification model, it measures the ability of the model to

distinguish between positive and negative examples. Finally, the Gini

coefficient aids in studying the distribution in model evaluation and is

particularly helpful when deciding between two classes.

Logistic Regression

Logit models are a class of models used to explore the relationship

of a dichotomous dependent variable to one or more independent

variables. (Gottman, J., & Roy, A., 1990). The logit model estimates

the probability that an event will happen or not (in our case, it

predicts if the customer will churn). In action, it shows to which

extent the independent variables will influence the event (churn) and in

what way.

The baseline model for this study is constructed based

on the study’s hypotheses deriving from the literature review and the

exploratory analysis. As a result, the baseline model consists of the

variables gender, age, income, relation length, electricity usage, gas

usage, contract length, and flexible contract. However, because contract

length and flexible contract are highly correlated and the inclusion of

both possibly causes multicollinearity problems, the flexible contract

is selected since it has a greater negative correlation with the

dependent variable.

The dataset is split into a training set

(75%) and a testing set (25%). The former is used for the estimation and

training of the model while the latter is for the evaluation of its

performance when a new dataset is introduced. The estimation of the

baseline model presents that most of the baseline variables are

statistically significant for predicting churn, except for gender and

age. This finding suggests evidence that the initial hypothesis which

states that males have a greater probability to churn is rejected,

similar to the hypothesis that age younger individuals have a greater

possibility of defecting.

# Logistic Regression

#Get a 75% estimation sample and 25% validation sample

set.seed(1234)

data$estimation_dataset <-rbinom(nrow(data), 1, 0.75)

estimation_dataset <- data[data$estimation_dataset == 1,]

validation_dataset<- data[data$estimation_dataset == 0,]

#Estimate the model using only the estimation sample

Logistic_regression2 <- glm(Churn ~ as.factor(Gender) + Age + Income + Relation_length + Electricity_usage +

Gas_usage + flexible_contract, family=binomial, data=estimation_dataset)

summary(Logistic_regression2)##

## Call:

## glm(formula = Churn ~ as.factor(Gender) + Age + Income + Relation_length +

## Electricity_usage + Gas_usage + flexible_contract, family = binomial,

## data = estimation_dataset)

##

## Coefficients:

## Estimate Std. Error z value Pr(>|z|)

## (Intercept) -3.608e+00 1.293e-01 -27.908 <2e-16 ***

## as.factor(Gender)1 -5.447e-03 3.997e-02 -0.136 0.892

## Age -1.927e-03 1.665e-03 -1.158 0.247

## Income -1.440e-04 7.633e-06 -18.859 <2e-16 ***

## Relation_length -1.040e-02 5.292e-04 -19.649 <2e-16 ***

## Electricity_usage 1.301e-03 4.031e-05 32.284 <2e-16 ***

## Gas_usage 1.083e-03 4.071e-05 26.601 <2e-16 ***

## flexible_contract1 1.910e+00 4.297e-02 44.446 <2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## (Dispersion parameter for binomial family taken to be 1)

##

## Null deviance: 20533 on 14813 degrees of freedom

## Residual deviance: 15469 on 14806 degrees of freedom

## AIC: 15485

##

## Number of Fisher Scoring iterations: 4#Create a new dataframe with only the validation sample

validation_dataset <- data[data$estimation_dataset==0,]

validation_dataset$Churn <- as.numeric(as.character(validation_dataset$Churn))

#Get predictions for all observations

predictions_model2 <- predict(Logistic_regression2, type = "response", newdata= validation_dataset)

fitcriteria_calculator(predictions_model2,validation_dataset$Churn)## HIT RATE INFORMATION:

## True Negatives: 1867

## False Negatives: 655

## True Positives: 1738

## False Positives: 625

##

## Hit rate (%): 73.79734

## Sensitivity (%): 72.6285

## Specificity (%): 74.91974

##

## TOP DECILE LIFT INFORMATION:

## TDL value: 1.56741

##

## GINI INFORMATION:

## GINI value: 0.6349836

## AUC INFORMATION:

## AUC value: 0.8174918

Observing the results, it becomes clear that flexible contract

is the most important attribute for predicting churn. Specifically,

having a flexible contract increases the risk of churn by 6.75 times

compared to a fixed contract. Income has a small decrease in odds per

unit increase (0.014%), while relation length reduces odds by 1% for

each unit increase. Both electricity usage and gas usage increase the

odds of churn by approximately 0.13% and 0.11% per unit increase,

respectively. The fit criteria for the base model were moderate as can

be seen in Table 2.

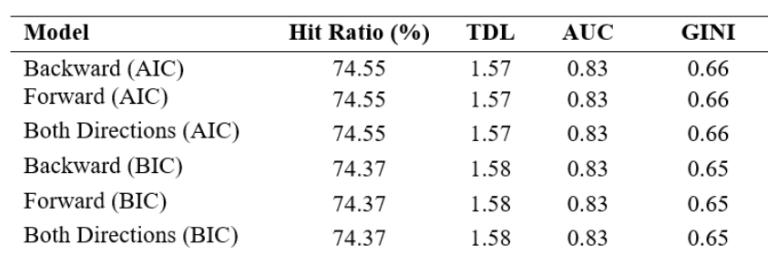

Stepwise Logistic

Instead of manually deciding the variables to include in the model,

as was done with the logistic regression method, Stepwise logistic

regression is utilized as a feature selection algorithm. The advantage

of this method is that it helps identify both important variables and

control variables. There are many types of stepwise regression: Forward,

Backward, or both. The process involves adding or removing a variable to

determine the extent to which it improves the model.

Decisions

are based on information criteria, such as the Akaike Information

Criterion (AIC) and Bayesian Information Criterion (BIC), along with

significance. The process continues until there is no substantial

improvement or worsening in the model.

BIC models were chosen,

whether using backward, forward, or both directions for model selection.

The Akaike Information Criterion tends to favor the complex models, in

contrast to the Bayesian Information Criterion, which showed a

preference for simpler models (Liu et al., 2023). The variables that

were identified through the stepwise regression process are: Income,

Relation_length, Start_channel, Email_list, Electricity_usage,

Gas_usage, and flexible_contract.

Stepwise Logistic Regression

performance metrics

# Stepwis Logistic Regression ----

## Model estimation ----

Logistic_regression_full <- glm(Churn ~ ., data = estimation_dataset, family = binomial)

Logistic_regression_null <- glm(Churn ~ 0, data = estimation_dataset, family = binomial)

### Backward Stepwise Logistic Regression

Logistic_regression_backward <- stepAIC(Logistic_regression_full,

direction="backward", trace = TRUE)

### Forward Stepwise Logistic Regression

Logistic_regression_forward <- stepAIC(Logistic_regression_null, direction="forward",

scope=list(lower=Logistic_regression_null, upper=Logistic_regression_full), trace = TRUE)

### Both Directions Stepwise Logistic Regression

Logistic_regression_both <- stepAIC(Logistic_regression_full,

direction="both", trace = TRUE)

## Bayesian Informationd Cruterion (BIC) ----

### Backward Stepwise Logistic Regression

Logistic_regression_backward_BIC <- stepAIC(Logistic_regression_full, direction="backward",

trace = TRUE, k = log(sum(data$estimation_dataset)))

### Forward Stepwise Logistic Regression

Logistic_regression_forward_BIC <- stepAIC(Logistic_regression_null, direction="forward",

scope=list(lower=Logistic_regression_null, upper=Logistic_regression_full),

trace = TRUE, k = log(sum(data$estimation_dataset)))

### Both Directions Stepwise Logistic Regression

Logistic_regression_both_BIC <- stepAIC(Logistic_regression_full, direction="both", trace = TRUE,

k = log(sum(data$estimation_dataset)))

## Predictions ----

# AIC Models

predictions_backward_AIC <- predict(Logistic_regression_backward, type = "response", newdata=validation_dataset)

predictions_forward_AIC <- predict(Logistic_regression_forward, type = "response", newdata=validation_dataset)

predictions_both_AIC <- predict(Logistic_regression_both, type = "response", newdata=validation_dataset)

# BIC Models

predictions_backward_BIC <- predict(Logistic_regression_backward_BIC, type = "response", newdata=validation_dataset)

predictions_forward_BIC <- predict(Logistic_regression_forward_BIC, type = "response", newdata=validation_dataset)

predictions_both_BIC <- predict(Logistic_regression_both_BIC, type = "response", newdata=validation_dataset)

## Fit Criteria ----

# AIC MODELS

fitcriteria_calculator(predictions_backward_AIC,validation_dataset$Churn)

fitcriteria_calculator(predictions_forward_AIC,validation_dataset$Churn)

fitcriteria_calculator(predictions_both_AIC,validation_dataset$Churn)

#BIC MODELS - Backward, Forward, Both

fitcriteria_calculator(predictions_forward_BIC,validation_dataset$Churn)

fitcriteria_calculator(predictions_backward_BIC,validation_dataset$Churn)

fitcriteria_calculator(predictions_both_BIC,validation_dataset$Churn)Decision Trees

The Decision Tree Classification model, specifically the CART

(Classification and Regression Tree) approach, is another technique

explored and evaluated. It comprises a supervised learning method

employed to classification tasks. This model operates by partitioning

the data in a way that minimizes impurity within each group. It creates

nodes by identifying and using the attributes that most significantly

reduce impurity until it is minimized. Decision tree models have the

capacity to discern and prioritize the most influential attributes

within a dataset for a specific task. Initially, the model is trained

using the training set, including all the variables and then it is

implemented on the testing set to evaluate its performance.

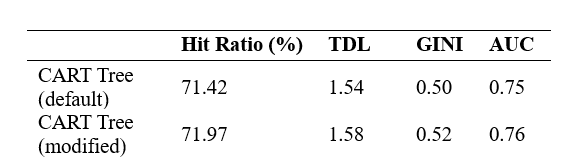

For

the aim of this study, two CART models are compared to determine the

superior performer. The first model utilizes default parameters, while

the second model is adjusted by reducing the complexity parameter from

0.01 to 0.008 and increasing the maximum depth to 4, thus allowing for a

more expansive tree. Performance metrics for both models are detailed in

Table 4. While the modified model shows slightly improved performance,

the default model is preferred due to concerns about overfitting. The

adjustments in the second model make the tree excessively specific,

potentially reducing its efficiency on a new dataset. Subsequently, the

default CART model is preferred.

CART Decision Tree

performance metrics

# CART tree

# Using the baseline variables

Cart_tree2 <- rpart(Churn ~ Age + Income + Relation_length + Electricity_usage +

Gas_usage + flexible_contract + Contract_length + Start_channel +

Email_list + Home_label, data=estimation_dataset, method="class")

predictions_cart2 <- predict(Cart_tree2, newdata=validation_dataset, type ="prob")[,2]

rpart.plot(Cart_tree2,extra = 106)

# Changing settings

newsettings1 <- rpart.control(minsplit = 100, minbucket = 50, cp = 0.008, maxdepth = 4)

Cart_tree3 <- rpart(Churn ~ ., data=estimation_dataset, method="class", control=newsettings1)

Cart_tree3_visual <- as.party(Cart_tree3)

# Save predictions

predictions_cart3 <- predict(Cart_tree3, newdata=validation_dataset, type ="prob")[,2]

# Performance Metrics (Remove hashtags to execute them)

# fitcriteria_calculator(predictions_cart2,validation_dataset$Churn)

# fitcriteria_calculator(predictions_cart3,validation_dataset$Churn)

For simplicity, only the selected CART model is

showcased.Examining the abobe decision tree, it is revealed that the

type of contract, specifically whether it is flexible or not, is the

primary determinant of predicting customer churn. This factor comprises

the root node of the decision tree. In particular, customers with

non-flexible contracts exhibit a 35% likelihood of churning. In

contrast, those with fl exible contracts present a 71% propensity to

churn.

As the decision tree further branches out, the next most

important variable is electricity usage. For customers with fixed

contracts and a yearly electricity consumption below 2223 kWh, the churn

probability is 22%. Conversely, the tree leads to another split which

includes relation length as a splitting rule. In this case, a customer

with a relationship greater than 37 months has a probability of almost

40% to defect, while customers with the shortest relationship, present a

probability of 58% to terminate their relationship with the company. On

the other hand, customers with a flexible contract and electricity usage

exceeding 1941 kWh have the greatest probability of defect, at 79%. The

last attribute presented in the tree is Gas usage, derived from

customers with electricity usage smaller than 1941kWh and indicates that

a customer has a 63% probability to churn when gas usage is larger than

979 cubic meters per month.

Overall, the tree model

comprehensively identifies which customer segments are more likely to

terminate their relationship with the company. In this case, it appears

that customers with flexible contracts and high energy consumption are

the segments that should be targeted for retention, as they present the

greatest probability of churn.

Random Forest

Random Forest is a specific type of ensemble model that builds a

collection of decision trees and combines their outputs. It is less

prone to overfitting compared to individual decision trees, as the

aggregation of multiple trees helps to smooth out individual errors.

Random Forest provides a measure of feature importance, indicating which

features contribute the most to the model’s predictions.

Two

random forests were implemented, one with no settings and the other with

700 trees. However for simplicity, only the results of the best

performing are presented. Models score almost the same on the fit

criteria, with no settings model scoring slightly better in the Hit

Ratio and the Gini Coefficient. The plot below shows that the most

important features are the same for both models. More specifically, the

top 5 variables, in order of importance, are the Electricity_usage,

Gas_usage, Relation_length, Income, and Start_channel.

# Random forest ----

estimation_dataset$estimation_dataset <- NULL

Random_forest1 <- randomForest(Churn ~ ., data=estimation_dataset, importance=TRUE)

predictions_forest1 <- predict(Random_forest1, newdata=validation_dataset, type ="prob")[,2]

# Extract variable importance measures

var_importance <- importance(Random_forest1)

importance_df <- data.frame(Variable = row.names(var_importance), Importance = var_importance[, 1])

# Plot variable importance using ggplot2

ggplot(importance_df, aes(x = Importance, y = reorder(Variable, Importance))) +

geom_bar(stat = "identity", fill = "lightblue") +

labs(x = "Importance", y = "Variable") +

ggtitle("Variable Importance") +

theme_minimal()

#Fit criteria Random_forest1

fitcriteria_calculator(predictions_forest1,validation_dataset$Churn)## HIT RATE INFORMATION:

## True Negatives: 1887

## False Negatives: 635

## True Positives: 1765

## False Positives: 598

##

## Hit rate (%): 74.75947

## Sensitivity (%): 73.54167

## Specificity (%): 75.93561

##

## TOP DECILE LIFT INFORMATION:

## TDL value: 1.580119

##

## GINI INFORMATION:

## GINI value: 0.6531703

## AUC INFORMATION:

## AUC value: 0.8265851Gradient Boosting

Boosting is an ensemble technique that strengthens a model by

sequentially integrating many weak learners, the decision trees, to form

a robust predictor. It enhances model accuracy by iteratively correcting

errors from previous models, with a special focus on data points that

are difficult to predict. A Gradient Boosting is applied in our analysis

that builds models in succession, each targeting the largest errors

until reaching a set accuracy threshold, improving generalization to new

data. Boosting works by taking the weighted sum of predictions from all

trees, leveraging the greedy nature of decision trees that make splits

based on immediate error reduction. By combining the predictions of

these trees, Boosting achieves a more accurate and reliable final

prediction.

Our model generates 10000 trees, the shrinkage

parameter lambda is 0.01 which is the learning rate, and the interaction

depth d represents the total number of splits to be performed. So here

each tree is a small tree with only 4 splits. The summary of the Model

gives a featureimportance plot. The two most important features that

explain the maximum variance in the data set are Electricity usage and

Contract length. The output shows a hierarchy of model determinants.

Electricity usage leads with 22.45%, as the paramount determinant.

Contract length (18.80%) and Gas usage (17.32%) follow closely and are

also very significant. Age, Home_label, and Home_age have minimal

effects (0.43%, 0.39%, 0.11%) and Gender, with no influence at all,

excluding it from the model’s key determinators. Partial dependence

plots are also implemented to show the relationship between the two most

important variables (Electricity usage and Contract length) with the

response variable (Churn).

estimation_dataset$estimation_dataset <- NULL

estimation_dataset$Churn <- as.integer(as.character(estimation_dataset$Churn))

# Model Estimation

boost_tree1 <- gbm(Churn ~ ., data=estimation_dataset,

distribution = "bernoulli", n.trees = 10000,

shrinkage = 0.01, interaction.depth = 4)

# Print the results

boost_tree1## gbm(formula = Churn ~ ., distribution = "bernoulli", data = estimation_dataset,

## n.trees = 10000, interaction.depth = 4, shrinkage = 0.01)

## A gradient boosted model with bernoulli loss function.

## 10000 iterations were performed.

## There were 13 predictors of which 13 had non-zero influence.# Best Iteration

best.iter <- gbm.perf(boost_tree1, method = "OOB",plot.it = FALSE)## OOB generally underestimates the optimal number of iterations although predictive performance is reasonably competitive. Using cv_folds>1 when calling gbm usually results in improved predictive performance.summary(boost_tree1, n.trees = best.iter, plotit = FALSE)## var rel.inf

## Electricity_usage Electricity_usage 22.60552485

## Contract_length Contract_length 18.67055470

## Gas_usage Gas_usage 17.25495653

## flexible_contract flexible_contract 13.63781098

## Relation_length Relation_length 10.15601191

## Income Income 8.09541464

## Start_channel Start_channel 3.75764901

## Email_list Email_list 2.96957237

## Province Province 1.84298000

## Age Age 0.47635397

## Home_label Home_label 0.39945627

## Home_age Home_age 0.12891768

## Gender Gender 0.00479708# Boosting predictions

predictions_boost1 <- predict(boost_tree1, newdata=validation_dataset, n.trees = best.iter, type ="response")

# Fit criteria

fitcriteria_calculator(predictions_boost1,validation_dataset$Churn)## HIT RATE INFORMATION:

## True Negatives: 1924

## False Negatives: 598

## True Positives: 1770

## False Positives: 593

##

## Hit rate (%): 75.61924

## Sensitivity (%): 74.74662

## Specificity (%): 76.44021

##

## TOP DECILE LIFT INFORMATION:

## TDL value: 1.6013

##

## GINI INFORMATION:

## GINI value: 0.6779132

## AUC INFORMATION:

## AUC value: 0.8389566Support Vector Machine

Support Vector Machines is a supervised machine learning algorithm

used for classification. It operates by constructing a hyperplane in a

feature space that distinctly separates instances belonging to different

classes. The goal is to find the hyperplane with the maximum margin,

which is the distance between the hyperplane and the nearest data points

from each class.

These nearest data points are referred to as

support vectors. The optimization process in SVM involves minimizing the

classification error while maximizing the margin, making it a robust

algorithm for both linear and non-linear classification tasks.

Additionally, SVM can handle high-dimensional data efficiently. Four

different kernel functions were conducted: Linear Kernerl, Polynomial

Kernel, Sigmoid Kernel, and Gaussian Radial Basis Function (RBF) (For

simplicity reasons only the best performing is presented). The variables

that were used are the ones that were used for the baseline model. Fit

criteria identified the Gaussian Radial Basis Function (RBF) as the

optimal model among the four, outperforming all others across all

criteria (Table 9). The only substantial plot is depicted in Figure 9,

illustrating the relationship between age and electricity usage. In

particular, the classification of people as churners increases when

their age increases and electricity consumption is above 3000, but after

their 60th year, the classification of churners decreases as they get

older.

## Gaussian Radial Basis Function (RBF) -----

svm_3 <- svm(Churn ~ Gender + Age + Income + Relation_length + Contract_length + Electricity_usage + Gas_usage + flexible_contract, data = data, importance=TRUE,

type = 'C-classification', probability = TRUE,

kernel = 'radial')

plot(svm_3, data, Electricity_usage~Age)

# Get predictions

predictions_svm3 <- predict(svm_3, newdata=validation_dataset, probability=TRUE)

predictions_svm3 <- attr(predictions_svm3,"probabilities")[,1]

# Fit criteria for Gaussian Radial Basis Function (RBF)

fitcriteria_calculator(predictions_svm3,validation_dataset$Churn)## HIT RATE INFORMATION:

## True Negatives: 1930

## False Negatives: 592

## True Positives: 1733

## False Positives: 630

##

## Hit rate (%): 74.98465

## Sensitivity (%): 74.53763

## Specificity (%): 75.39062

##

## TOP DECILE LIFT INFORMATION:

## TDL value: 1.622482

##

## GINI INFORMATION:

## GINI value: 0.6467897

## AUC INFORMATION:

## AUC value: 0.8233948Managerial Conclusion

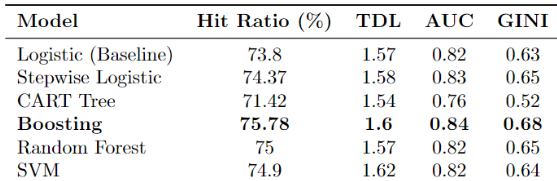

It is determined from the models that the variables that have the most substantial influence on churning are service usage (electricity & gas usage), contract length, flexible contract, and relation length. Gradient boosting is chosen as the best model for the Dutch Energy Supplier, based on the performance metrics. The performance metrics suggest that the Boosting model exhibits the highest predictive capability, representing a significant enhancement over the baseline model. More specifically, it has the highest scores in fit criteria with a Hit Ratio of 75.78%, TDL of 1.6, AUC of 0.84, and Gini Coefficient of 0.68.

After the execution of Partial Dependence Plots, where the relation and direction between important variables and target variable are revealed, it is concluded that service usage influence positively on churn. In other words, as the service usage increases, the probability of churn increases. Consequently, the hypothesis that service usage potentially leads to lower churn rates is rejected in our study. Regarding the contract length it is found that customers possessing extended contract terms demonstrated diminished churn rates, aligning with the hypothesis outlined in the literature review. As for the hypothesis on relationship length positing a negative impact on the probability of churn, the results confirm the anticipated negative relationship.

Performance metrics for all models

Thus, in order to enhance customer retention, the Dutch energy

supplier is recommended to develop and promote energy-efficiency

programs for customers with higher usage, which can lead to cost savings

and increased customer satisfaction. Furthermore, it is advisable to

establish loyalty programs that reward long-term customers, such as

offering discounts or exclusive services to those with extended contract

terms. This will help in strengthening the company’s relationship with

the customers. Lastly, more attention has to be given to the creation of

blog posts and educational videos to help the customers understand the

long-term benefits and potential savings of staying with the

company.

Appendix

1. R libraries needed

To successfully execute this project, the following R libraries

are required:

# Loading necessary libraries

library(tidyr)

library(corrplot)

library(ggplot2)

library(dplyr)

library(ROCR)

library(randomForest)

library(reshape2)

library(e1071)

library(rpart)

library(rpart.plot)

library(partykit)

library(MASS)

library(gbm)

library(neuralnet)2. Detailed dataset description

- Customer_ID: a unique customer identification number.

- Gender: a dummy variable indicating if the customer who signed the

contract is male (0) or female (1).

- Age: the age of the customer in years.

- Income: the monthly income of the customer’s household in euros.

- Relation_length: the amount of months the customer has been with the

firm.

- Contract_length: the amount of months the customer still has a

contract with the firm. Zero

means the customer has a flexible contract, i.e., (s)he can leave anytime without paying a

fine. If the contract is more than zero months, the customer can still leave, but has to pay a

fine when leaving. - Start_channel: indicating if the contract was filled out by the

customer on the firm’s website (“Online”) or by calling up the firm

(“Phone”).

- Email_list: indicating if the customer’s email address is known by the firm (1=yes, 0=no).

- Home_age: the age of the home of the customer in years.

- Home_label: energy label of the home of the customer, ranging from A (good) to G (bad).

- Electricity_usage: the yearly electricity usage in kWh.

- Gas_usage: the yearly gas usage in cubic meters.

- Province: the province where the customer is living.

- Churn: a dummy variable indicating if the customer has churned (1)

or not (0)

3. Fit Criteria Custom Function

The fitcriteria_calculator function assesses binary classification model performance. It calculates hit rate, sensitivity, specificity, top decile lift (TDL), and plots a lift curve. Additionally, it computes the Gini coefficient and the area under the ROC curve (AUC), providing a comprehensive evaluation of the model’s predictive accuracy and discriminative capacity * Execute this custom function in the beggining of the script.

# Custom function calculator for fit criteria

fitcriteria_calculator <- function(predict, IV) {

tablebase <- ifelse(predict > .5, 1, 0)

# HIT RATE CALCULATIONS

hitrate_table <- table(IV, tablebase, dnn = c("Observed", "Predicted"))

hit_rate <- ((hitrate_table[1,1] + hitrate_table[2,2]) / sum(hitrate_table)) * 100

sensitivity <- (hitrate_table[2,2] / (hitrate_table[2,2] + hitrate_table[1,2])) * 100

specificity <- (hitrate_table[1,1] / (hitrate_table[1,1] + hitrate_table[2,1])) * 100

# TDL CALCULATIONS (10 levels)

decile_ntile <- ntile(tablebase, 10)

decile_table <- table(IV, decile_ntile, dnn = c("Observed", "Decile"))

tdl <- (decile_table[2,10] / (decile_table[1,10] + decile_table[2,10])) / mean(IV)

# LIFT CURVE PLOT

pred <- prediction(predict, IV)

perf <- performance(pred, "tpr", "fpr")

plot(perf, xlab = "Cumulative % of observations", ylab = "Cumulative % of positive cases", xlim = c(0, 1), ylim = c(0, 1), xaxs = "i", yaxs = "i", main = "Lift Curve") + abline(0, 1, col = "red")

# GINI AND AUC CALCULATIONS

auc_perf <- performance(pred, "auc")

auc <- as.numeric(auc_perf@y.values)

gini <- auc * 2 - 1

# Output

cat('HIT RATE INFORMATION:', '\n', 'True Negatives:', hitrate_table[1,1], '\n', 'False Negatives:', hitrate_table[1,2], '\n', 'True Positives:', hitrate_table[2,2], '\n', 'False Positives:', hitrate_table[2,1], '\n',

'\n', 'Hit rate (%): ', hit_rate, '\n', 'Sensitivity (%): ', sensitivity, '\n', 'Specificity (%): ', specificity, '\n', '\n',

'TOP DECILE LIFT INFORMATION:', '\n', 'TDL value:', tdl, '\n', '\n',

'GINI INFORMATION:', '\n', 'GINI value:', gini, '\n',

'AUC INFORMATION:', '\n', 'AUC value:', auc)

}

Note that the `echo = FALSE` parameter was added to the code chunk to prevent printing of the R code that generated the plot.